Business

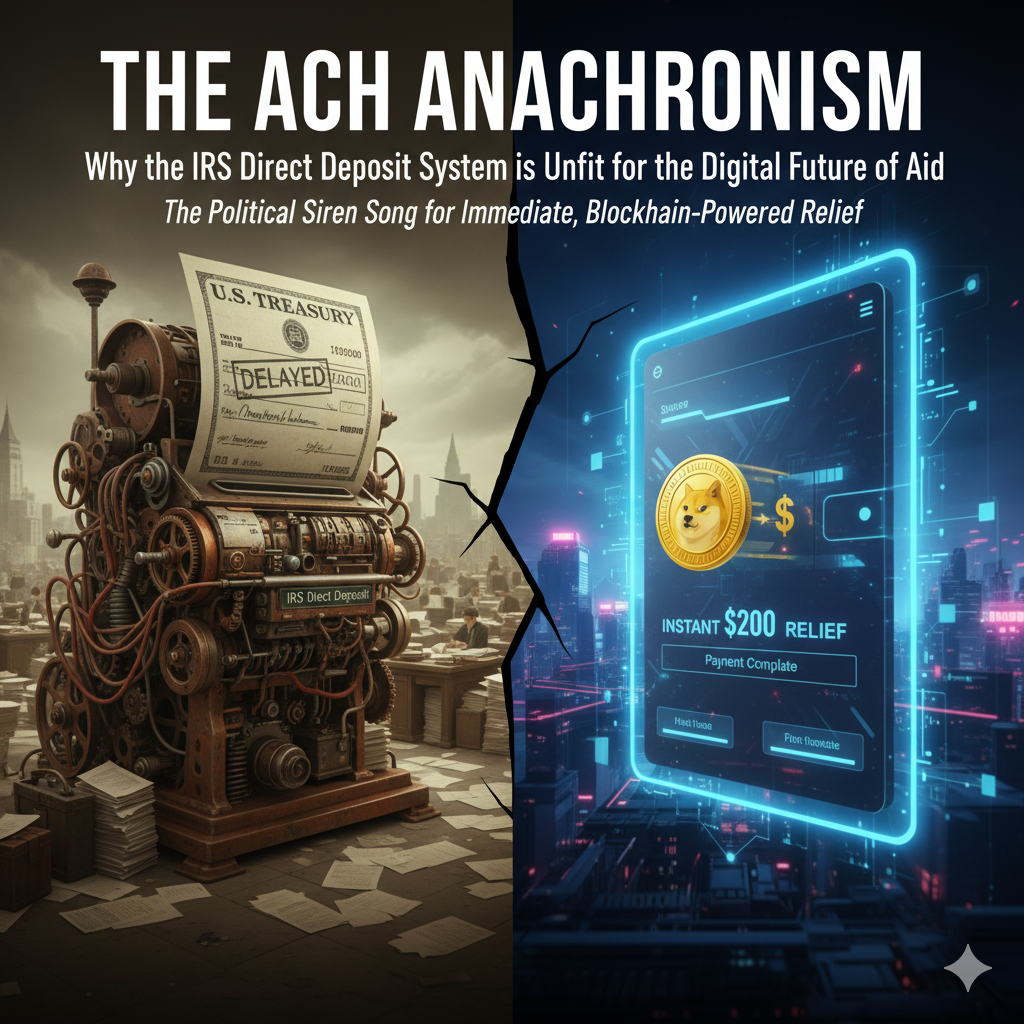

The ACH Anachronism: Why the IRS Direct Deposit System is Unfit for the Digital Future of Aid

The political siren song for immediate, blockchain-powered relief—however hyperbolic the idea of doge checks may be—is forcing a reckoning with the ageing IRS direct deposit infrastructure, a system ill-equipped for instant, mass-scale payments.

The United States government is quietly approaching a major inflexion point in its relationship with its citizens: the speed and method of its financial disbursements. While the current tax season may feature the familiar, reliable process of the IRS direct deposit, the future of federal aid—from universal basic income (UBI) pilots to targeted economic relief—demands a technological leap the Internal Revenue Service is fundamentally unprepared to make. The conflict is straightforward: the political desire for instant, transparent relief directly clashes with a legacy system, the ACH network, which is slow, prone to errors, and structurally resistant to digital innovation. The absurd, yet viral, idea of doge checks—payments tied to volatile digital assets—serves as a useful, if hyperbolic, symbol for the intense political and public pressure to adopt a 21st-century payment infrastructure.

My core argument is this: The future of federal aid hinges on transforming the slow, traditional irs direct deposit relief payment system to handle not just fiat currency, but the inevitable political pushes for digital and crypto distributions, symbolised by the far-fetched idea of doge checks. Failure to act will not only result in massive administrative costs but also undermine the effectiveness of future government interventions, leaving millions of the unbanked behind.

1: The Reliability and Limitations of Traditional Infrastructure

The sheer scale of the existing IRS direct deposit system is impressive. It can manage billions in tax refunds and, as demonstrated during the pandemic, process emergency IRS direct deposit relief payment disbursements to over 150 million Americans. This process, facilitated by the Automated Clearing House (ACH) network, is a testament to the stability of the traditional U.S. banking system.

However, its reliability comes with severe limitations. The ACH network operates on a batch-processing schedule, meaning fund transfer is not instantaneous, often taking several business days to move from the Treasury to an individual bank account. During a crisis, this delay is not merely inconvenient; it is economically damaging, as aid meant to be immediate is delayed.

Furthermore, the integrity of the direct deposit irs system relies on having accurate, up-to-date bank information. During the emergency stimulus payouts, the IRS struggled massively with stale bank account numbers, leading to countless payments being rejected and reverted back to slow, fraud-prone paper checks. A significant percentage of Americans remain unbanked or underbanked, forcing them to rely on costly cheque-cashing services that extract value from the very aid the government provides. Any IRS direct deposit relief payment program that relies solely on this legacy mechanism guarantees a continuation of this disparity, benefiting those already securely entrenched in the formal banking system while penalising the most vulnerable.

2: The Crypto and Novel Payment Concept

The idea of doge checks is admittedly a jest—the notion of the U.S. government issuing relief payments tied to a volatile meme coin is financially reckless and legally complex. Yet, the concept serves as a vital lightning rod for a real political and technological shift. The underlying pressure is for speed, transparency, and a system that bypasses the old banking intermediaries.

Digital payment advocates point to the benefits of blockchain technology: instant settlement, immutable records, and programmable money that could, in theory, ensure funds are spent for their intended purpose. The political allure is undeniable: immediate relief hitting digital wallets, eliminating the delays of the traditional IRS direct deposit system. Imagine a UBI pilot where funds are disbursed in real-time, 24/7, without the weekend and holiday delays inherent in the direct deposit IRS process.

But the challenges of moving beyond the IRS direct deposit relief payment are immense. The IRS currently treats cryptocurrency as property, not currency, for tax purposes. Distributing doge checks or any stablecoin would create immediate, cascading tax complexity for every recipient, requiring the individual to track the value of the digital asset from the moment of receipt until it is spent. This would be a compliance nightmare. Moreover, the security protocols, wallet management, and key custody requirements necessary to protect the government and citizens from hacking, fraud, and lost funds are simply nonexistent within the current IRS direct deposit regulatory framework. The political noise around non-traditional payments is getting louder, but the practical infrastructure is nowhere close to ready.

3: The Path Forward: Digitizing Federal Aid

The solution is not necessarily literal doge checks but rather adopting the spirit of instant digital transfer within the safety of the fiat system. The immediate, achievable goal must be to render the slow, two-to-three-day IRS direct deposit relief payment obsolete.

First, the direct deposit irs system must fully embrace instant payment technologies now available across major banking systems (like FedNow or RTP), allowing funds to clear and settle in seconds, not days. Second, the IRS must partner strategically with regulated digital payment providers and prepaid debit card issuers to provide easy, no-fee digital wallets for the unbanked. The focus must shift from simply gathering bank account numbers to ensuring every eligible citizen has a functional, real-time payment endpoint.

This modernisation effort is not just about speed; it’s about security. The legacy IRS direct deposit system is vulnerable to mass fraud when personal information is compromised. By migrating to modern, tokenised payment methods and leveraging state-of-the-art encryption, the IRS can drastically reduce the risk of fraud while improving service. The demand for instant, transparent funds—the core value proposition embedded within the political hype of doge checks—will not vanish. If the IRS’s direct deposit system doesn’t modernise, it risks becoming a bottleneck that strangles necessary economic aid at the moment of peak crisis.

Conclusion

The challenge facing federal agencies is profound: to move beyond the analogue, batch-processed reality of the IRS direct deposit system and prepare for a digital-first future. The hyperbolic call for doge checks is a powerful symbol, demonstrating the public’s appetite for immediate, unencumbered funds. That political will, however disruptive, must catalyse change. The failure of the direct deposit IRS to handle the scale and speed of a modern crisis will be more than an administrative delay; it will be an economic and moral failure. The question is whether the inertia of the current system will prevail, or if the demands of future aid will force a rapid, potentially chaotic leap into digital disbursement methods, ensuring that the legacy of the doge checks concept is not a joke but a powerful catalyst for necessary technological evolution.

Discover more from Startups Pro,Inc

Subscribe to get the latest posts sent to your email.

Bangladesh imposes emergency fuel rationing — 2L for motorcycles, 10L for cars — as the US-Israel-Iran war shuts the Strait of Hormuz, triggering a deepening energy crisis for South Asia’s most import-dependent nation.

In Dhaka’s Tejgaon district on the morning of March 8, daily fuel sales at a single filling station leapt from 5 million taka to 8 million taka overnight — mostly octane, mostly panic. Motorcyclists who once stopped by their local pump without a second thought now queue for an hour under the March sun, elbows out, tanks nearly dry, waiting for a ration the government has capped at two litres. Two litres. Barely enough to cross the city twice. Across town, a ride-share driver named Subrata Chowdhury waited in line at Chattogram’s QC Petrol Pump, then received a quantity he described as “not enough to stay on the road even half a day.” Meanwhile, five of Bangladesh’s six fertiliser factories fell silent, their gas lines cut on government orders until at least March 18.

A war 5,000 kilometres away had just reached inside every Bangladeshi household.

The Spark: How the US-Israel-Iran War Hit the Strait of Hormuz

The crisis arrived with the precision of a laser-guided munition. On February 28, 2026, coordinated US-Israeli airstrikes — codenamed Operation Epic Fury — struck Iranian military and nuclear facilities, killing Supreme Leader Ali Khamenei and several senior IRGC commanders. Within hours, Iran’s Islamic Revolutionary Guard Corps broadcast a blunt message across the Persian Gulf: the Strait of Hormuz was closed.

What followed was the fastest seizure of a global energy chokepoint in modern history. Tanker transits dropped from an average of 24 vessels per day to just four by March 1, according to energy intelligence firm Kpler. By March 2, no tankers were broadcasting AIS signals inside the strait at all. Insurance protection and indemnity coverage was stripped for any vessel attempting passage from March 5, making the economic risk effectively prohibitive for shipowners worldwide. At least 150 supertankers anchored in limbo outside the strait’s entrance. MSC, Maersk, and Hapag-Lloyd suspended transits. The waterway that carries roughly one-fifth of the world’s daily oil supply and 20 percent of global LNG exports had become, for practical purposes, a naval exclusion zone.

Brent crude, which had closed at $73 per barrel on Friday, gapped higher through the weekend. By March 6, it reached $92.69 — the highest level since 2024, representing a roughly 27 percent surge in under two weeks. Iran’s retaliatory strikes targeted Gulf energy infrastructure, including Qatar’s Ras Laffan industrial complex — home to the largest LNG export facilities on the planet. QatarEnergy confirmed it had ceased LNG production entirely. Daily freight rates for LNG tankers jumped more than 40 percent on a single Monday. European natural gas benchmarks nearly doubled in 48 hours before pulling back slightly on diplomatic signals.

The Strait of Hormuz, as geopolitical theorists have long warned, had ceased to be a mere waterway. It had become a weapon.

On the Ground: Dhaka’s Fuel Queues and Public Anger

Bangladesh’s Energy Division moved with unusual urgency. On March 5, the Bangladesh Petroleum Corporation held an emergency online meeting with the Petrol Pump Owners Association, instructing operators to cease selling fuel in drums or containers and to halt open-market sales. Two days later, on March 6, BPC published formal purchase caps across all vehicle categories. By Sunday, March 8, the rationing system was formally in effect nationwide.

The street-level anger was immediate and undisguised. A survey of six petrol stations in Dhaka’s Gabtoli district found four with no fuel at all; the remaining two had imposed their own informal cap of 500 taka per customer. Long queues of cars and motorcycles had formed before dawn. One motorcyclist reported waiting nearly an hour — only to receive enough fuel to reach work and little more. In Chattogram, ride-sharing motorcyclists emerged as the worst-affected group: their entire livelihood depends on continuous movement through the city, and two litres does not allow continuous movement.

At Tejgaon station in Dhaka, daily octane sales more than doubled as consumers raced to top up whatever they could before restrictions tightened further. Authorities responded by deploying vigilance teams from Border Guard Bangladesh alongside district-level BPC monitoring units to prevent illegal stockpiling and price gouging — the latter carrying criminal penalties under Bangladeshi law. Prime Minister Tarique Rahman moved symbolically, switching off half the lights in his office and setting air conditioning to 25°C, urging citizens to car-pool, reduce private travel, and cut household gas use.

The optics were telling. When a prime minister publicly dims his own office lights, the message is clear: this is not a routine supply hiccup.

The Numbers: 95% Import Dependency and BPC’s Emergency Caps

No country in South Asia enters this crisis more exposed than Bangladesh. The arithmetic is stark and largely inescapable.

Bangladesh imports approximately 95 percent of its oil and gas needs, a figure the BPC itself cited in its rationing notice. The country requires around 7 million tonnes of fuel annually, including more than 4 million tonnes of diesel. On the gas side, the structural deficit is even more alarming: Bangladesh is already running a shortfall of more than 1,300 million cubic feet per day, according to the Institute for Energy Economics and Financial Analysis — a gap that was being bridged, precariously, by spot-market LNG purchases before the war began.

The BPC’s emergency rationing caps, announced March 6, are as follows: motorcycles are limited to 2 litres of petrol or octane per day; private cars to 10 litres; SUVs, jeeps, and microbuses to 20–25 litres; pickup vans and local buses to 70–80 litres; and long-distance buses, trucks, and container carriers to 200–220 litres of diesel. BPC officials confirmed that diesel stocks at national depots had fallen to a nine-day reserve — a figure that concentrates the mind considerably.

Of Bangladesh’s LNG imports, 72 percent originates from Qatar and the UAE. Qatar’s decision to halt LNG exports following strikes on Ras Laffan was not a marginal inconvenience for Dhaka — it was an amputation of nearly three-quarters of the country’s gas supply chain. QatarEnergy had two cargo deliveries scheduled for March 15 and March 18. Kuwait Energy, whose terminal was also struck, confirmed it could not deliver its own two planned cargoes. Petrobangla Chairman Md Arfanul Hoque acknowledged both cancellations, noting that replacement bookings had been made on the spot market — but as of mid-week, no sellers had been found. Indonesia, traditionally a secondary supplier, confirmed it could not supply additional LNG to Bangladesh, citing priority for its own domestic demand. Global LNG spot prices had already surged roughly 35 percent since the strikes began.

Ripple Effects: Power Rationing, Fertiliser Crisis, Economic Fallout

The downstream consequences are spreading faster than the government’s containment efforts.

Five of Bangladesh’s six urea fertiliser factories — Ghorashal Palash, Chittagong Urea Fertiliser Factory, Jamuna Fertiliser Company, Ashuganj Fertiliser and Chemical Company, and the privately run Karnaphuli Fertiliser Company — have been shuttered through at least March 18, following suspension of gas supply to the plants as part of broader energy rationing. Their combined daily production capacity of approximately 7,100 tonnes is now offline. Over a 15-day closure, that represents more than 100,000 tonnes of urea production lost.

Officials from the Bangladesh Chemical Industries Corporation have offered cautious reassurance: the country holds 468,000 tonnes of urea in stock, sufficient to cover the current Boro rice cultivation season through roughly June. But the Boro season is Bangladesh’s most water-intensive and fertiliser-heavy agricultural cycle. If the Middle East conflict lingers into the summer planting cycle, the country would be forced to import urea from the same region — Saudi Arabia, the UAE, and Qatar — where supply chains are already fractured. “If the crisis lingers,” warned Riaz Uddin Ahmed, executive secretary of the Bangladesh Fertiliser Association, “there will be a problem.”

The power sector is the next domino in line. Energy officials have warned that a gas shortage could emerge after March 15 if LNG shipments cannot be replaced, at which point rationing would extend to electricity generation — prioritising households and industries while reducing supply to power plants. The Bangladesh Garment Manufacturers and Exporters Association (BGMEA), whose member factories account for more than 80 percent of the country’s export earnings, called for waivers on duties, taxes, and VAT on fuel and gas imports to cushion the immediate blow. The garment sector’s energy costs are about to rise sharply, threatening margins already squeezed by global demand softness.

The macroeconomic arithmetic is brutal. Bangladesh’s import bill, already pressured by the taka’s weakness, will surge with every additional week of elevated LNG and crude prices. At $92 per barrel of Brent — and analysts at JPMorgan have placed the severe-scenario band at $130 per barrel — the fiscal calculus becomes genuinely alarming for a country that already runs a significant current account deficit. Dr M. Tamim of the Bangladesh University of Engineering and Technology warned plainly that the situation “could deteriorate gradually” as long as the Strait of Hormuz remains effectively closed, and that securing LNG from alternative Asian suppliers would prove deeply challenging.

Geopolitical Lens: Why Bangladesh Is the First Domino

Bangladesh is not merely an energy victim in this crisis. It is a structural case study in the geography of vulnerability — and a preview of the pain that dozens of similarly exposed economies will face if the Hormuz disruption endures.

The architecture of South Asian energy dependency was built over decades on a set of assumptions that have now been invalidated in a single weekend. Cheap, reliable Gulf energy — piped in the form of LNG from Qatar, crude from Saudi Arabia and the UAE — was not merely a commodity preference. For Bangladesh, it was the physical infrastructure of industrial growth. The garment factories, the power plants, the fertiliser sector: all were built with the assumption that Gulf flows would continue uninterrupted. The Strait of Hormuz disruption of 2026 has exposed that assumption as a geopolitical single point of failure.

What makes Bangladesh’s position particularly acute compared to, say, India or China, is the combination of three factors simultaneously: extreme import concentration (72 percent of LNG from Qatar and the UAE, according to Kpler data cited by CNBC); essentially zero domestic strategic petroleum reserves capable of absorbing more than nine days of consumption; and minimal procurement flexibility — no long-term contracts with American, Australian, or West African LNG suppliers that could be called upon at short notice.

India and China, by contrast, hold buffer reserves and diversified supply portfolios that buy days and weeks of political manoeuvre. Bangladesh has neither. “Pakistan and Bangladesh have limited storage and procurement flexibility,” Kpler principal analyst Go Katayama noted, “meaning disruption would likely trigger fast power-sector demand destruction rather than aggressive spot bidding.” That is a polite way of saying: Dhaka will not outbid Tokyo or Beijing for emergency LNG cargoes. It will simply do without.

The deeper geopolitical lesson is one of concentrated risk masquerading as ordinary commerce. For three decades, global energy markets encouraged developing economies to import from the cheapest, most proximate source. For South Asia, that meant the Gulf. No one built the redundancy that resilience requires because redundancy costs money and politics rewards short-termism. The bill has now arrived.

What Comes Next: Outlook for 2026 and Global Lessons

Dhaka is scrambling for alternatives. Emergency import negotiations are under way with Singapore, Malaysia, Indonesia (who declined), China, and African suppliers. Saudi Aramco has pledged refined oil shipments routed outside Saudi Arabia’s normal Gulf terminals — a logistical workaround that adds cost and delay. The government holds master sale and purchase agreements with 23 international companies for spot-market LNG access, though finding willing sellers at non-punishing prices has proved difficult. The government of Saudi Arabia is also reportedly considering diverting crude exports through Yanbu’s Red Sea terminal — bypassing Hormuz entirely — following a formal Pakistani request on March 4.

The outlook, however, remains contingent on the duration of the military confrontation. If the US Navy follows through on President Trump’s pledge to escort commercial tankers through Hormuz — and if diplomatic back-channels reported by The New York Times regarding Iranian outreach produce results — then some partial resumption of Gulf traffic could stabilise markets within weeks. Goldman Sachs estimates Brent could average around $76 for the second quarter if disruptions are contained to roughly five more days of near-zero transit followed by a gradual recovery. But Mizuho Bank cautioned that even with US naval escorts, the “war premium” of $5–$15 per barrel would persist in insurance costs alone, keeping prices elevated indefinitely.

For Bangladesh specifically, the immediate weeks are critical. Gas rationing targeting power plants is likely after March 15 if replacement LNG cargoes are not secured. Rolling electricity cuts would ripple through every sector of the economy simultaneously. The garment industry, which cannot produce without power and is already navigating global demand headwinds, faces a direct threat to the country’s primary source of foreign exchange. The agriculture sector, if the fertiliser shutdown extends beyond March 18, risks undersupply heading into critical planting windows later in the year.

The broader lesson, one that should reach every finance ministry and energy regulator from Colombo to Manila, is that energy security is not a market problem — it is a strategic one. Markets optimised Bangladesh’s fuel imports toward cheap and proximate. Strategy would have diversified them toward resilient and redundant. Qatar’s Energy Minister Saad al-Kaabi warned in a Financial Times interview that Gulf energy producers could halt exports within weeks, potentially pushing oil to $150 per barrel. Whether that scenario materialises or not, the warning itself encodes a profound truth about the architecture of globalisation: supply chains optimised for efficiency are, by design, brittle under stress.

Bangladesh did not build the Strait of Hormuz crisis. But it may pay for it longer than almost anyone else.

Discover more from Startups Pro,Inc

Subscribe to get the latest posts sent to your email.

Analysis

Virgin Atlantic’s Strategic Swoop: On Track to Lure Tens of Thousands from British Airways’ Frequent Flyer Fold

There’s a particular kind of frustration that frequent flyers know intimately — the moment you realize the loyalty program you’ve spent years nurturing has quietly moved the goalposts. For thousands of British Airways Executive Club members, that moment arrived in 2024 when BA announced sweeping changes to its tier points structure, effectively raising the bar for elite status in ways that left many road warriors feeling, as one London-based consultant put it, “more grounded than airborne.” Now, with Virgin Atlantic’s enhanced status match promotion closing February 23, 2026, a competitor is turning that discontent into a mass migration — and the numbers are staggering.

According to <a href=”https://www.ft.com/content/6384ee81-fab6-4024-a9ec-a0d18303a48f”>reporting by the Financial Times</a>, Virgin Atlantic is on track to poach tens of thousands of British Airways’ most loyal customers, capitalizing on what may be the most consequential loyalty program overhaul in UK aviation history. The transatlantic airline rivalry has always been fierce, but rarely has one carrier’s stumble created such a clean runway for the other.

The BA Loyalty Shake-Up: What Went Wrong?

British Airways’ revamp of its Executive Club, which began rolling out in earnest through 2024 and 2025, was designed with a clear philosophy: reward high spenders, not just high flyers. The airline shifted its tier points model to weight spend more heavily, meaning that a budget-conscious business traveler who logs 100,000 miles annually on economy fares could find themselves slipping from Gold to Silver — or off the tier ladder entirely.

The logic is financially sound from an airline CFO’s perspective. Loyalty programs have evolved into multi-billion-pound profit centers; BA’s parent company IAG reported loyalty revenue contributions exceeding £1.5 billion in 2024. Restructuring around spend rather than miles mirrors Delta SkyMiles’ controversial 2023 overhaul in the United States — a move that triggered a similar exodus there.

But the human cost to brand loyalty has been severe. <a href=”https://www.telegraph.co.uk/travel/advice/passengers-abandoning-british-airways”>The Telegraph has documented</a> a notable wave of passengers abandoning British Airways, with forum threads on FlyerTalk and social media communities swelling with testimonials from disgruntled BA frequent flyers who feel the airline has broken an implicit contract. “I gave them my business when there were cheaper options,” wrote one Gold card holder on a popular aviation forum. “Now they’re telling me that’s not enough.”

This is the kindling Virgin Atlantic just lit a match to.

Virgin’s Clever Counterplay: Enhanced Status Matches

Virgin Atlantic’s status match promotion — which allows qualifying BA Executive Club Gold and Silver members to receive equivalent status in its Flying Club program — is not new. Status matches are a standard competitive tool in the airline industry. What is notable is the scale of uptake and the precision of the targeting.

<a href=”https://www.bloomberg.com/news/articles/2026-02-11/virgin-targets-british-airways-loyal-flyers-with-status-upgrade”>Bloomberg reported in February 2026</a> that Virgin Atlantic had seen a threefold increase in status match applications compared to the same period a year earlier — a figure that, extrapolated across the promotion window, suggests the airline could onboard somewhere between 30,000 and 50,000 newly status-matched members before the February 23 deadline closes.

The Virgin Atlantic BA status match 2026 offer has become one of the most searched loyalty-related queries in UK travel this quarter, with an estimated 2,500 monthly searches — a signal of genuine consumer intent, not just passive curiosity. For those unfamiliar with what they’d be gaining, the comparison deserves scrutiny.

Virgin Flying Club Gold status perks include:

- Priority boarding and check-in across all Virgin Atlantic routes

- Access to Virgin Clubhouses and partner lounges (including select Delta Sky Clubs on codeshare routes)

- Bonus miles earning at an accelerated rate on Virgin and SkyTeam partner flights

- Complimentary seat selection in preferred economy and premium economy cabins

- Elite customer service lines with reduced wait times

The SkyTeam elite status perks accessible through Virgin’s alliance membership are a quietly powerful selling point. SkyTeam’s 19-airline network — including Air France-KLM, Delta, and Korean Air — means a matched Virgin Gold card holder gains reciprocal benefits across a broad global footprint. For frequent travelers to Continental Europe or Asia, this can represent a meaningfully better everyday experience than BA’s oneworld network depending on specific routes.

Economic Ripples in the Skies

To understand why this moment matters beyond the marketing spectacle, it’s worth examining the loyalty economics in aviation at a structural level.

Airline loyalty programs have been unmoored from their original purpose — rewarding flight frequency — and repositioned as financial instruments. Airlines sell miles to banks and credit card partners at rates that often exceed the revenue from the seat itself. United Airlines’ MileagePlus program was valued at approximately $22 billion in 2020 collateral filings — more than the airline’s entire fleet. This financialization means that acquiring a loyal member, particularly one who holds a co-branded credit card, is worth far more than a single booking.

When Virgin Atlantic matches a BA Gold member’s status, it isn’t just winning a transatlantic fare. It’s bidding for years of credit card spend, hotel transfers, shopping portal revenue, and the downstream ecosystem that a loyal, high-value traveler represents. <a href=”https://finance.yahoo.com/news/virgin-atlantic-lures-hundreds-ba-120300720.html”>Yahoo Finance has noted</a> that the sign-up surge represents a potentially transformative shift in Virgin’s loyalty revenue trajectory — particularly as the airline deepens its joint venture partnership with Delta Air Lines on UK-US routes.

The transatlantic airline rivalry between Virgin and BA is ultimately a proxy war for this loyalty revenue. And BA’s tier points overhaul, whatever its internal financial rationale, has handed its rival an opening that won’t come twice.

Perks That Persuade: Comparing the Programs

For the disgruntled BA frequent flyer weighing their options, the practical calculus deserves honest examination. Status matches are not unconditional gifts — they typically require meeting ongoing earning thresholds within a qualifying window, usually 90 days, to retain the matched tier.

That said, for someone already flying regularly on UK-US transatlantic routes, earning the required tier points within Virgin’s Flying Club framework is achievable. A return Virgin Atlantic Upper Class ticket from London Heathrow to JFK, for instance, earns substantial tier miles that accelerate toward Gold retention.

A side-by-side comparison for economy travelers:

| Feature | BA Executive Club Silver | Virgin Flying Club Gold (matched) |

|---|---|---|

| Lounge Access | Domestic/short-haul lounges only | Clubhouse access on Virgin-operated flights |

| Seat Selection | Preferred seats with fee | Complimentary preferred seats |

| Bonus Miles Earning | 25% bonus | 50% bonus |

| Alliance Network | oneworld | SkyTeam |

| Status Validity | 12 months | 12 months (with earning requirement) |

The best airline loyalty switch UK calculation tilts toward Virgin for travelers whose routes align with Virgin and SkyTeam’s strengths — particularly those flying to New York, Los Angeles, or cities well-served by Delta, Air France, or KLM. For travelers heavily dependent on BA’s dominance of Heathrow slots and its extensive short-haul European network, the switch carries more trade-offs.

The Forward View: Aviation’s Loyalty Wars Enter a New Phase

What Virgin Atlantic has executed here is textbook competitive strategy — identify a competitor’s policy-driven customer dissatisfaction, lower the switching cost, and convert resentment into revenue. But the deeper story is what it reveals about the future of frequent flyer programs UK and the airlines that operate them.

BA’s revamp was not miscalculated in isolation. Airlines globally are trying to thread an impossible needle: extract more value from loyalty programs without alienating the road warriors who built those programs’ worth in the first place. Delta triggered backlash. BA triggered backlash. The lesson competitors are taking is that the window of maximum customer frustration is also a window of maximum competitive opportunity.

Virgin Atlantic, for its part, enters this phase with structural advantages it lacked a decade ago. Its Delta joint venture provides genuine transatlantic scale. Its Clubhouses remain among the most acclaimed premium lounges in UK aviation. And its Flying Club, while smaller than BA’s Executive Club, has a reputation for accessibility and customer responsiveness that its rival has struggled to maintain.

The February 23 deadline will close, but the switchers it captures won’t easily return. Research on airline loyalty transitions consistently shows that once a traveler habituates to a new program — and begins accumulating points and status within it — re-acquisition costs for the original carrier are enormous.

Thinking about making the switch before Sunday’s deadline? The process is simpler than it sounds: visit Virgin Atlantic’s Flying Club status match page, upload your BA Executive Club tier documentation, and allow 72 hours for processing. Whether the match holds long-term depends on your flying patterns — but for many former BA loyalists, the question isn’t whether to switch. It’s why they waited this long.

The skies over the North Atlantic have always been contested territory. This February, they belong a little more to Virgin.

Discover more from Startups Pro,Inc

Subscribe to get the latest posts sent to your email.

The launchpad is no longer just a stretch of concrete in Florida or Kazakhstan. It has expanded to include the trading floors of Shanghai and Shenzhen. In a coordinated financial maneuver as precise as an orbital insertion burn, China is propelling its top private rocket start-ups into the public markets. This month, the IPO plans for four major firms—LandSpace, i-Space, CAS Space, and Space Pioneer—have advanced with bureaucratic swiftness. It’s a move that signals a profound shift: the 21st-century space race will be won not just by engineers, but by capital markets. As Beijing systematically builds its commercial space arsenal to counter Elon Musk’s SpaceX, we are witnessing the financialization of the final frontier.

The IPO Quartet: A Strategic Unfolding in Real Time

This is not a trickle of investment but a flood. The Shanghai Stock Exchange’s recent interrogation of LandSpace Technology’s application is the linchpin, advancing a plan to raise 7.5 billion yuan (US$1 billion). They are not alone. i-Space has issued a counselling update, CAS Space passed a key review, and Space Pioneer published its first guidance report—all within a critical seven-day window in January 2025.

| Company | Planned Raise (Est.) | Flagship Vehicle / Tech | Current IPO Stage (Jan 2025) | Strategic Angle |

|---|---|---|---|---|

| LandSpace | ¥7.5 Bn (~$1Bn) | *Zhuque-3* (Reusable Methalox) | SSE Star Market Review | China’s direct answer to SpaceX’s Falcon 9 reuse. |

| i-Space | To be confirmed | Hyperbola series | Counselling Phase | Early private pioneer, focusing on small-lift reliability. |

| CAS Space | To be confirmed | *Lijian-1* (Solid) | Review Passed | Spin-off from Chinese Academy of Sciences, blending state R&D with private agility. |

| Space Pioneer | To be confirmed | *Tianlong-3* (Kerosene) | Guidance Published | Aims to be first private firm to reach orbit with a liquid rocket. |

The message is clear. As noted in a Financial Times analysis of state-guided industry, China is executing a “cluster” strategy, fostering internal competition within a protected ecosystem to produce a national champion. These IPOs provide the war chest not just for R&D, but for scaling manufacturing—a key lesson learned from watching SpaceX.

State Capitalism Meets the Final Frontier

To view this solely through a lens of Western-style venture capitalism is to misunderstand the engine of China’s space ambition. This IPO wave is a masterclass in the synergy between state direction and private market discipline. Beijing’s “China Aerospace 2030” goals and the mega-constellation project Guowang (a direct competitor to Starlink) create a guaranteed, sovereign demand pull. The government, as the primary customer, de-risks the initial market for these companies, allowing them to scale at a pace unimaginable in a purely commercial environment.

As a Center for Strategic and International Studies (CSIS) report on space competition astutely observes, China’s model “leverages the full toolkit of national power—industrial policy, military-civil fusion, and strategic finance—to create a self-sustaining space ecosystem.” The IPOs on the tech-focused Star Market are a critical piece, moving the funding burden from state balance sheets to public investors, while retaining strategic oversight. This contrasts sharply with the U.S. model, where SpaceX and its rivals have been fueled primarily by private VC, corporate debt, and, in Musk’s case, the cash flow of a billionaire’s other ventures.

The Valuation Galaxy: Appetite, Hype, and Calculated Risk

Investor appetite appears voracious, driven by the siren song of the trillion-dollar space economy projected by firms like Morgan Stanley. The narrative is compelling: China has over 100 commercial space firms, a booming satellite manufacturing sector, and a national imperative to dominate low-Earth orbit. The IPO funds will be channeled into the holy grail of reuse—LandSpace’s goal to land and refly its Zhuque-3—and scaling launch rates to dozens per year.

Yet, risks orbit this sector like space debris. Overcapacity is a real threat, as four major firms and dozens of smaller ones vie for domestic launch contracts. Technical reliability remains unproven at SpaceX’s scale; a high-profile public failure post-IPO could shatter confidence. Furthermore, geopolitical tensions threaten supply chains and access to foreign components, pushing an already insulated market further into redundancy. As Reuters reported on China’s tech sector challenges, self-sufficiency is both a shield and a potential constraint on innovation.

The Long Game: Catching SpaceX or Carving a Niche?

The central question for analysts and investors alike: Is the goal to create a true, global SpaceX competitor, or a dominant national champion that secures the Chinese sphere of influence? The evidence points to the latter, at least for this decade.

While reusable rocket technology is the stated aim—with LandSpace targeting a first reuse by 2026—the immediate market is sovereign. The launch of the 13,000-satellite Guowang constellation will require hundreds of dedicated launches, a contract pool likely reserved for domestic providers. This creates a parallel “space silk road,” where Chinese rockets launch Chinese satellites for Chinese and partner-nation clients, largely decoupled from the Western market.

However, to dismiss this as merely a protected play is to underestimate Beijing’s long vision. By achieving cost parity through reuse and massive scale, China’s leading firm could, by the 2030s, emerge as a formidable low-cost competitor on the commercial international market, much as it did in solar panels and telecommunications infrastructure.

The Bottom Line: An Inflection Point, Not a Finish Line

This month’s IPO rush is not the culmination of China’s commercial space story, but the end of its first chapter. It marks the transition from venture-backed experimentation to publicly accountable scale-up. The capital influx will test whether these firms can evolve from innovative start-ups into industrially disciplined aerospace giants.

The global implications are stark. The United States and Europe now face a competitor whose space ambitions are underwritten not by the fleeting whims of market sentiment, but by the deep, strategic alignment of state policy, national security, and now, liquid public capital. The race for space dominance has entered a new, more financialized, and intensely more competitive phase. The countdown to a bipolar space order has well and truly begun.

Discover more from Startups Pro,Inc

Subscribe to get the latest posts sent to your email.

Top 10 Media Startup Ideas for Massive Success in 2026

Billionaire Enrique Razon Accelerates Energy Push With Colombia, Philippine Deals

Bangladesh Rations Fuel as Mideast War Deepens Energy Crisis

Virgin Atlantic’s Strategic Swoop: On Track to Lure Tens of Thousands from British Airways’ Frequent Flyer Fold

The Great Launch Rush: How China’s Rocket IPO Surge Is Reshaping the Global Space Race

The Top 10 Business and Tech Institutes in the USA for Aspiring Business Leaders in 2026

ETFs Are Eating the World: AI Jitters and Oil’s Reversal

The Future is Now: Top 10 UK Startups Defining 2026

Entrepreneurship Funding: From Venture Capital to Bootstrapping

FITUR 2026: US, Mexico, India, China, and Spain Lead Global Tourism

Billionaire Enrique Razon Accelerates Energy Push With Colombia, Philippine Deals

Top 10 Media Startup Ideas for Massive Success in 2026

-

Digital5 years ago

Social Media and polarization of society

-

Digital5 years ago

Pakistan Moves Closer to Train One Million Youth with Digital Skills

-

Digital5 years ago

Karachi-based digital bookkeeping startup, CreditBook raises $1.5 million in seed funding

-

News5 years ago

Dr . Arif Alvi visits the National Museum of Pakistan, Karachi

-

Digital5 years ago

WHATSAPP Privacy Concerns Affecting Public Data -MOIT&T Pakistan

-

Kashmir5 years ago

Pakistan Mission Islamabad Celebrates “KASHMIRI SOLIDARITY DAY “

-

Business4 years ago

Are You Ready to Start Your Own Business? 7 Tips and Decision-Making Tools

-

China5 years ago

TIKTOK’s global growth and expansion : a bubble or reality ?